Broadband Competition is Thriving Across America

Additional regulation of broadband providers, particularly smaller providers, is unwarranted and would be counterproductive

An ACA Connects White Paper | June 23, 2022

UPDATE:

New FCC Data Confirms ACA Connects’ Report’s Finding That Broadband Competition is Thriving

The Share of U.S. Households with Access to Multiple Providers of Fast Broadband Continues to Grow Rapidly

Findings

In this White Paper, ACA Connects uses FCC data to demonstrate that fixed broadband competition is thriving in the United States and will become only more intense in the near future. Specifically, the vast majority of U.S. households either already have or soon will have access to at least two providers of fast and reliable fixed broadband service. Furthermore, even for those households that may not have access to two such providers in the near future, most of these households either already have or soon will have access to a subsidized provider of fixed broadband service whose prices and other terms of service are already subject to regulatory oversight. Thus, there is no need to impose additional heavy-handed common-carrier-style regulation on fixed broadband providers as a whole. Doing so would yield few, if any, tangible benefits while discouraging entry, investment and innovation, to the detriment of consumers. Finally, a strong case can be made for exempting smaller providers from any such regulation even if it were to be imposed on larger providers.

Introduction and Executive Summary

Decades ago, the federal government established a two-prong approach to bringing fast and reliable broadband service that meets consumer needs to all Americans: enable and encourage entry and competition in a light-touch regulatory environment; and, where the economics were too challenging, subsidize the provision of service. Despite the success of this approach, there have been recent calls for the federal government to abandon its light-touch regulatory treatment of broadband service and replace it with more heavy-handed common-carrier-style regulation.1 Such a reversal is not only unwarranted but would be counterproductive, as it would yield few tangible benefits while discouraging entry, investment and innovation, to the detriment of consumers.

In this White Paper, ACA Connects first demonstrates that current policies have been an enormous success: most households have a choice of at least two providers offering fast and reliable service and the trends show that even more households will have choice of additional providers in the near future. We then demonstrate that in many broadband markets served by only a single provider, that the provider is constrained by existing regulatory forces applied through high-cost support mechanisms. Finally, we explain that common-carrier-style regulation would be particularly burdensome on smaller providers and that the marginal gain from imposing this additional regulation on smaller providers would be vanishingly small if the additional regulation were already being imposed on larger providers. Therefore, smaller providers should be exempted from any additional regulation even if it were to be imposed on larger providers.2

Broadband Competition Is Widespread and Increasing Rapidly

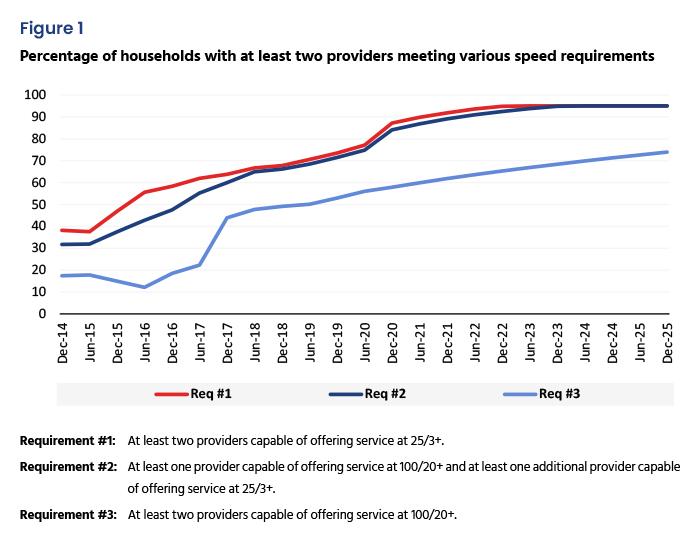

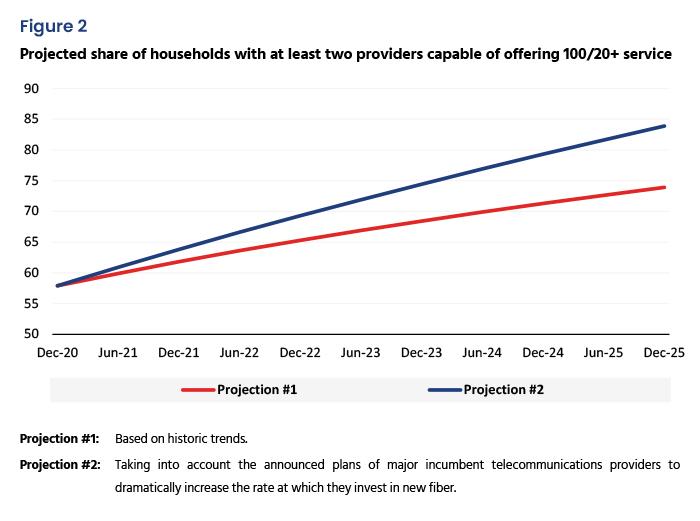

Broadband markets in the United States are by and large competitive today, and the trends indicate that competition is becoming more widespread. Federal Communications Commission (FCC or Commission) data show that the share of U.S. households that have access to multiple providers of fast broadband is already very large and is increasing rapidly. Based simply on projecting historic trends, we estimate that by December 2025, well over 90% of households will have access to at least one broadband provider offering 100/20+ service and at least one additional provider offering 25/3+ service.3 We also project that approximately 74% of all households will have access to at least two broadband providers both offering 100/20+ service. Furthermore, these projections based solely on extrapolating historic trends are likely conservative, given the announced plans of most major incumbent telecommunications providers to dramatically accelerate the pace of their investments in fiber-to-the-premises (fiber) infrastructure over the next five years. Taking these already-announced plans for accelerated investments in fiber into account, we project that approximately 84% of all households will have access to at least two providers both offering 100/20+ service by December 2025. Therefore, the potential benefits of greater regulation (lower prices and faster speeds in areas without sufficient competition) would be limited, while the harms of such regulation (reduced investment incentives, reduced efficiency incentives, reduced innovation and reduced experimentation with new business models) would be felt throughout the entire United States.

Even Most Markets with a Single Provider Do Not Require Additional Regulation

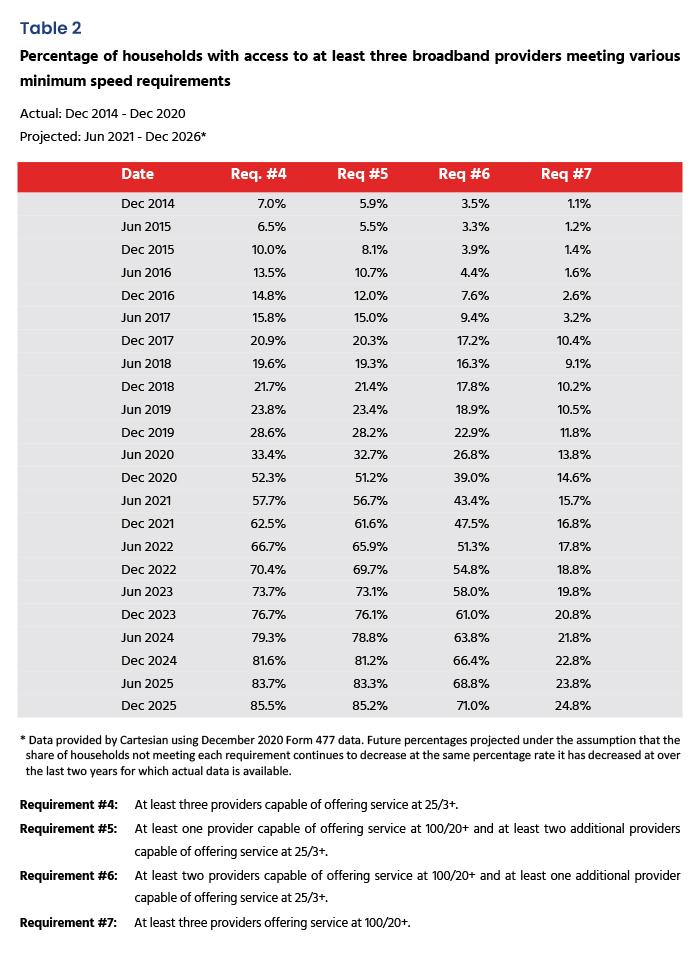

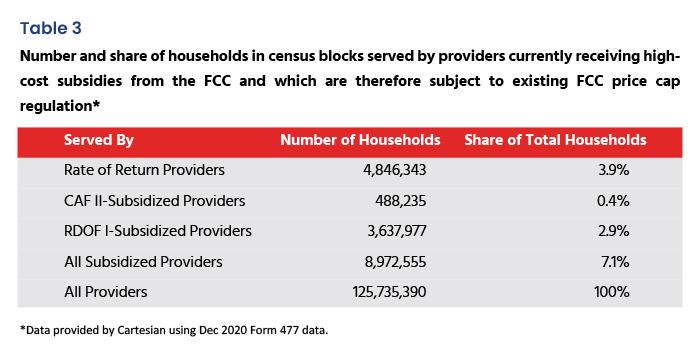

While the share of households without access to at least two providers of fast broadband is already small and shrinking rapidly, even this metric overstates the need for common-carrier-style regulatory intervention. The FCC is engaged in substantial programs to subsidize the provision and operation of broadband service in less dense high-cost areas of the country, and, through these programs, it already has — and exercises — authority to regulate most aspects of the services, including the prices charged and speeds provided, offered by these subsidized providers. Approximately 7% of all U.S. households are in areas served by a subsidized, and therefore already-regulated broadband provider. Furthermore, the number of these households will increase dramatically over the next few years as states begin to distribute funds provided under the Broadband Equity Access and Deployment (BEAD) program and various federal stimulus programs. Many of the U.S. households without two fast broadband providers are located in these less dense and high-cost areas of the country. Thus, a significant share of households without access to at least two providers of fast broadband are either already being served by or will soon be served by a subsidized and regulated provider, thus further diminishing the benefits of imposing additional regulation on all broadband providers.

Smaller Providers Should Be Exempted from Any Additional Regulation

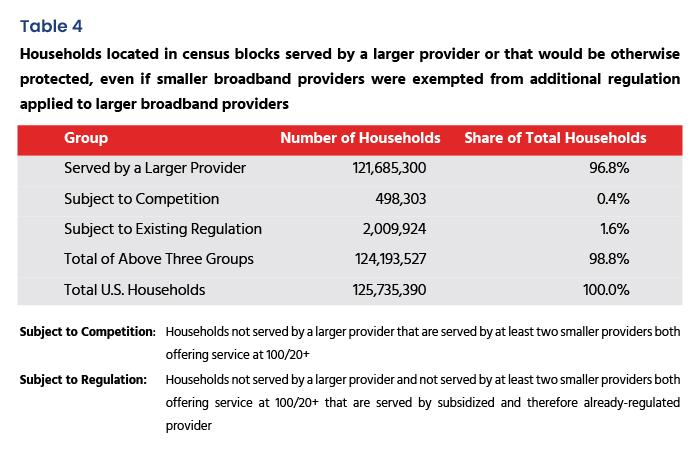

There are several reasons not to apply common-carrier-style regulation to smaller broadband providers, even if such regulation were to be imposed on larger providers. First, smaller providers, many of which are family businesses, cooperatives or municipal entities, simply do not have the financial sophistication and administrative capability to comply with a complex set of new regulatory requirements and procedures without incurring significant additional costs. Customers of these firms will ultimately bear a substantial fraction of these cost increases. Moreover, if common-carrier-style regulation were applied only to larger providers, regulatory pressure would still be placed on smaller providers to the extent that they serve an area that is also served by a larger provider and thus would have to compete for customers with the larger regulated provider. Approximately 97% of U.S. households are in areas served by at least one larger broadband provider. Furthermore, many of the remaining 3% of households are located in areas where there are at least two smaller providers already offering service at 100/20+ (and are thus already protected by competition) or in areas where there is currently a provider of broadband service receiving FCC high-cost subsidy support (that is already subject to regulatory oversight because it is subsidized). Thus, the share of households that would potentially benefit from extending additional regulation to smaller providers is very small and will decrease further.

Download White Paper

Download Full White Paper

Press Release

Vast Majority of U.S. Households Benefit from Robust Fixed Broadband Competition That Will Grow and Become More Intense In Near Future, A New ACA Connects’ Study Finds

White Paper's Tables and Figures

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

1 By “common carrier style regulation,” we mean regulation that includes regulation of the prices that providers charge for their services as well as other terms of service. Calls for common carrier style regulation have also occurred at the state level.

2 Similar arguments apply to both fixed broadband providers and mobile broadband providers. However, in this paper, ACA Connects focuses only on providers of fixed broadband. Unless otherwise indicated, this paper will use the term “broadband” to refer to “fixed broadband.”

3 Broadband speeds are typically reported as two numbers, x/y, where the first number is download speed in megabits per second (Mbps) and the second number is upload speed in Mbps. We will use x/y+ to denote service that is at least as fast as x/y. See the body of this paper for an extensive discussion of the minimum number of competitors necessary to justify relying on competitive forces rather than common carrier style regulation to organize the provision of broadband service to consumers, and the minimum speed of service that these carriers should be capable of offering to meet the needs of consumers. For purposes of these projections, we include providers using cable, DSL, fiber or fixed wireless technologies. To be conservative, we exclude providers using satellite or other technologies because capacity limitations may limit the competitive impact of providers using these technologies.